To state the blatantly obvious, debt sucks. It’s not just the emotional drain of living with a bank-sized elephant on your shoulders as you live pay check-to-pay check, it also effects your future.

Being in debt ruins your credit rating, and when your credit rating is in the red, you’re squandering your chances of buying a house in Sydney.

It’s not that you’re a bad person, or even an uneducated person. And really, I’d wager to say that your debt is not entirely your fault. They don’t offer classes in school about how to pay off credit cards, and last time I checked, interest rates weren’t on the high school curriculum.

Retraining yourself

Here’s a hard truth for you – the banks don’t care if you get out of debt. Actually, that’s not true. They do care, because they don’t want you to pay off your debt. They want you to keep your credit card debt, so that they can get more of your money. That’s why when you go to see a financial advisor at a bank, you’ll likely find that they’ll push their products on to you rather than giving you practical advice for paying off your debt fast.

The only way to do this is to educate yourself. And I want to stress here that I’m not a financial advisor – I’m a mortgage broker in Sydney. The advice I give here is general in nature and doesn’t take into account every financial situation possible. But I do know a thing or two about how first homebuyers can ensure they become a low risk gamble for a potential mortgage lender, so here’s some general, but nonetheless essential, advice for improving your financial fitness.

How to pay off your debt and get approved for that home loan

To pump up your finances for the rest of the year, you need to overhaul your routine. These next steps that follow will help you do just that.

See what shape your debt is in

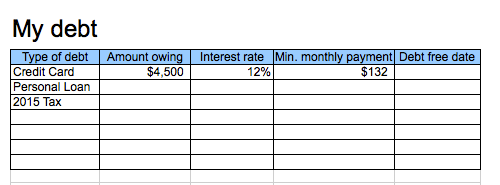

Do you know how much debt you actually have? Including your credit cards, personal loans, unpaid taxes, and HECS debt? If not, it’s time to get an excel spreadsheet, and make a chart that looks like this.

This chart is designed to help you figure out how much you owe, and when you can expect to pay it all off by if you pay the bare minimum each month.

Paying off debt – it’s a marathon, not a sprint!

Whichever debt has the highest interest rate, attack that one first. Don’t be persuaded by the banks to take out yet another personal loan to consolidate your debt, because this will affect your credit rating. Anytime you apply for credit and get declined, this goes as a mark against your credit history, which can negatively affect your credit score.

Don’t miss payments or default on your bills – or else!

When you’re working hard and putting your money towards paying off your debt, it can be tempting to put off that water bill or that phone bill for a week or two. But don’t. Just don’t. Every time you’re late with a bill, a service provides laughs like Freddy Kruger and then lets the credit rating agencies in on the joke. And that joke is you, because your credit rating just took another hit. Ouch.

Shape up your day-to-day routine

For anyone trying to pay off debt fast and then save for a mortgage, budgeting is a cold hard truth. Start using a budgeting app – like Pocket Expense – to divide your expenses into categories and then track what you spend on a daily basis. The results might just surprise you!

Strengthen your affordability

When you pay your mortgage lender a visit, they have a list of criteria to assess whether you can actually service this loan. Here’s a list of questions they’ll drill you on – make sure you read that post before you’re in their office!

One of the most major criteria for affordability is income. If you have a steady and reliable income, you’ll improve your chances of getting your mortgage application approved. This might mean a full-time job for you, or at least industry stability if you’re self-employed. If you’re self-employed, most lenders will require at least two year’s worth of tax returns to make their decision.

It’s hard work, but it’s worth the sweat

Overhauling your physical fitness is not an overnight job – and neither is strengthening your financial fitness muscle. Like any training program, it takes time, energy and dedication. But no one ever regretted a good workout, right?